Reconciling a Card Transaction from End to End: Mission Impossible Without Granularity

Publié

Le 04/06/2025, par :

- Anne Marie Diom

Sections

Card payment flows often give the illusion of being under control. The amounts seem to match, daily totals are consistent, and internal tools show everything consolidated “per day.”

But in reality? A single transaction may exist in 4 to 5 different forms, depending on the system you’re looking at:

- Raw data from the POS terminal,

- An authorization record in the switch,

- A clearing entry in the card network file,

- A suspense account entry in 472,

- A settlement movement in account 512.

👉 Without granularity, it’s nearly impossible to match them all together.

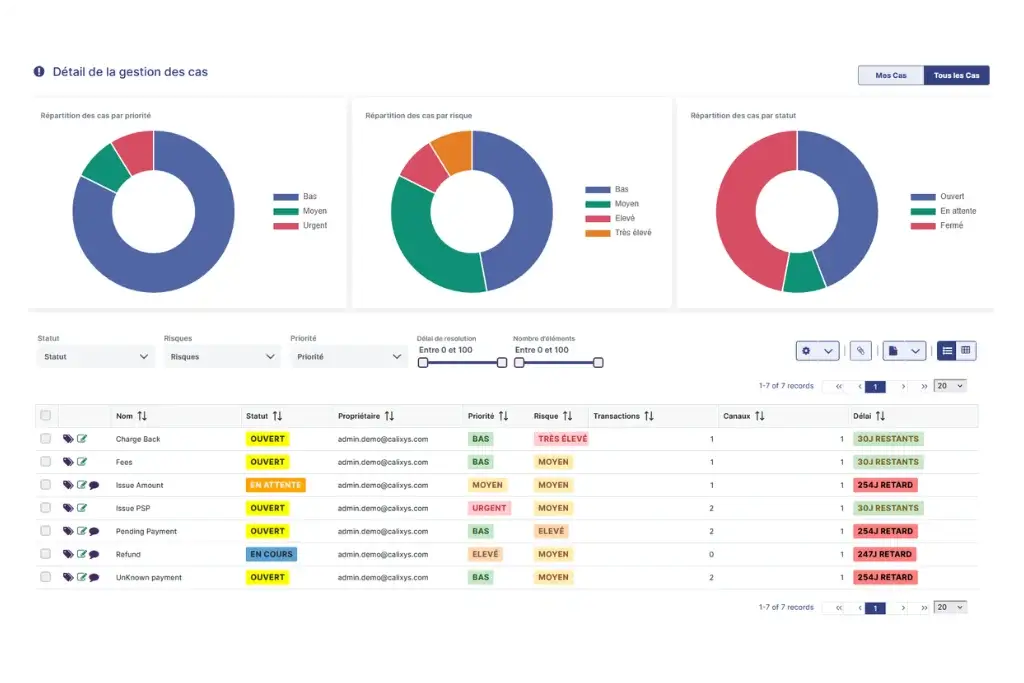

This challenge primarily concerns banks—their finance departments, internal control teams, monetics back-office units, and compliance officers. These are the stakeholders who manage, process, and justify massive volumes of transactions across fragmented systems on a daily basis.

When Aggregated Views Hide Real Anomalies

Let’s take a simple example: you record €100,000 in card sales on Monday, and receive €100,000 in settlements the following Thursday. At first glance, all seems well.

And yet… a rejected transaction, a duplicate, or a partial settlement could be hiding in that total.

Aggregated reconciliation creates an illusion of accuracy.

➡️ Only a transaction-level analysis allows you to detect real discrepancies, even when global totals align.

The consequences ?

- Undetected variances that disrupt justifications in accounts 472 and 512

- Extended time spent during closings

- Difficulties explaining anomalies during audits

- Degraded trust in the quality of financial data and internal reporting

Granularity: The Essential Lever to Trace Each Transaction

Reconciling a transaction isn’t about comparing two totals:

it’s about precisely matching the right records across different sources—each with its own formats and logic.

The most reliable matching keys?

- PAN (Primary Account Number)

- STAN (System Trace Audit Number)

- Exact date and timestamp

- Amount and currency

- Terminal ID or channel of origin

These identifiers are rarely altered throughout the transaction lifecycle. They provide a stable and unique link for tracing a transaction across systems: POS, switch, card network, clearing file, accounting system… That consistency makes them the foundation of secure reconciliation.

Granularity enables you to reconstruct the full journey: from the POS to the 512 ledger entry, passing through authorization, clearing, and final settlement.

It’s also becoming a compliance requirement: regulators increasingly expect banks to provide full transaction-level traceability and robust audit trails.

Use Cases: What Granularity Makes Visible

Here are five examples of anomalies that only transaction-level reconciliation can uncover:

🔁 A duplicated transaction: same amount, same day, but two different STANs. Impossible to catch in aggregated views.

❌ An unflagged rejection: a declined transaction that still appears in the clearing file.

📉 A partial settlement: €100 authorized, €85 settled—with no explanation or alert if you’re working with daily totals.

🔄 Acquirer/Issuer mismatch: the transaction is logged on the wrong interbank flow, making cash reconciliation unclear.

📊 A split transaction: some e-commerce operations are broken into multiple entries across PSPs or settled in different batches.

Conclusion: Without Granularity, You're Managing by Estimation

In a world where payment volumes are exploding, systems are siloed, and regulatory expectations are rising, granularity is no longer a luxury—it’s a necessity.

This message is especially for banks, monetics teams, back-office departments, CFOs, and internal control managers who must reconcile and justify thousands of multi-source transactions daily.

Reconciling in “summary mode” is like flying blind.

A platform like XREC enables you to trace, match, and justify each transaction in real time, consolidating your card, banking, and accounting data into one reliable workflow.